Download Report

Download Report

We use cookies to improve your experience

Please click "Accept" to help us improve its usefulness with additional cookies.

Learn about our use of cookies

Cookie Policy

In the Domestic Financial Ecosystem, many Central Banks have managed significant inroads in understanding the frameworks for introducing Central Bank Digital Currencies. The natural evolution of this Digital Form of Money will be towards easing Cross Border Money Transfer activities.

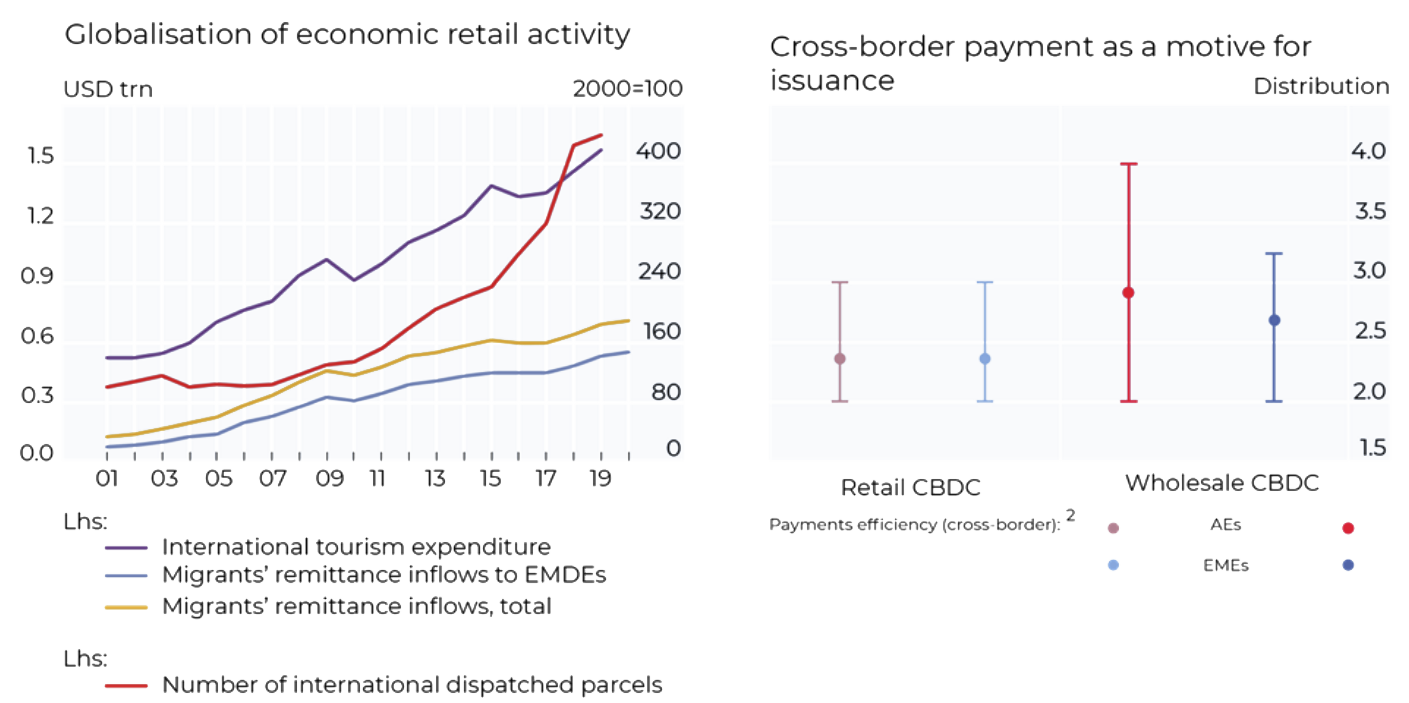

Cross-border remittances are ever more essential for economies, particularly for transactions that support tourism, e-commerce, and remittances, which have increased considerably over the last few years. However, such payments are often plagued by the following difficulties:

• They can get slow

• The overall process is opaque; and

• It is expensive; the cost of remitting money to some Jurisdictions can get as high as 10%

The United Nations, World Bank, and the IMF are working towards improving cross-border payment systems, and it is a priority for globally coordinated policy efforts. A multi-year G20 "roadmap" is coordinating efforts (G20 FMCBG (2020) and CPMI (2020)). The United Nations mandates to bring the cost of remittance to less than 3% by the year 2030.

The Bank of International Settlements, through its innovation hub, is working rigorously upon the Cross-border payment methods. It is evident that there are inefficiencies in the process, and investing in new technologies can assist in optimizing International Remittances. Research suggests that Cross-border payments can be made more straightforward and transparent by deploying several methods such as:

• Interoperating central bank digital currencies (CBDCs),

• Forming multi-CBDC (mCBDC) arrangements,

• Improving compatibility, and

•Inter-linking or integrating national payment systems.

The Bank for International Settlements (BIS) acknowledges the potential for multi-CBDC (mCBDC) systems to develop the synergy of CBDCs across borders. This paper will examine the following points.

• Dimensions of payment system interoperability

•How they could feature in mCBDC arrangements; and,

•Potential benefits on offer.

Today, the global cross-border payment landscape is at the center of several trends that could fundamentally change competitive dynamics, such as:

• Shifting regulatory and sanctions frameworks;

• Accelerating international commerce (retail as well as corporate); and

• Especially, changing customer demands..

Instead of creating a global private sector global stable coin, the Multi-CBDC arrangements offer to foster a diversity of convertible national currency and strengthen the monetary sovereignty in the digital age.

Cross-border payments are still dependant on interoperability and experience friction.

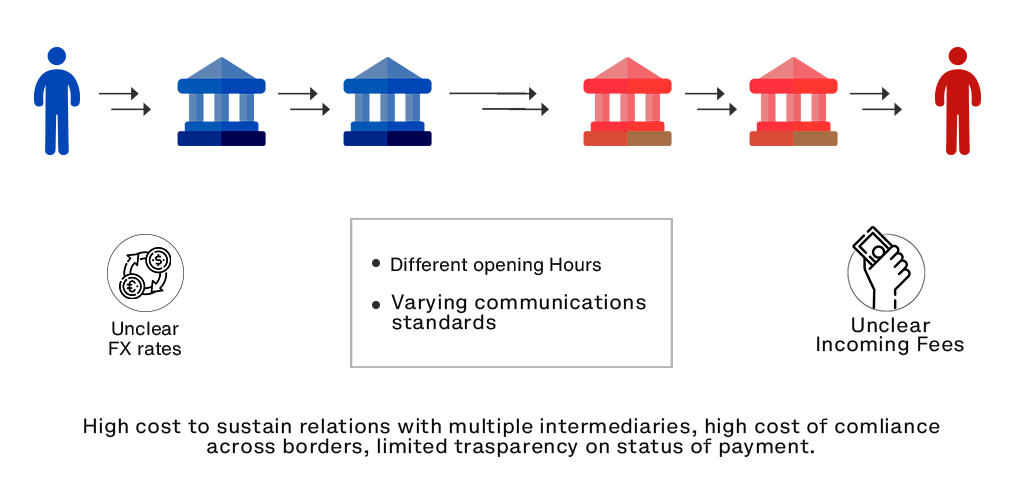

Multi-currency, cross-border payments are more complex than their domestic counterparts. A large number of cross-border payments are settled through correspondent arrangements. Moreover, these arrangements enhance the number of touchpoints having a direct impact on cost increase.

Furthermore, a particular Jurisdiction's Systems will naturally prioritize local participants in their design, which is a significant hurdle in the fluid processing of Global Remittance Payments. For example, payments systems use domestic message standards and have opening hours matching regional financial markets.

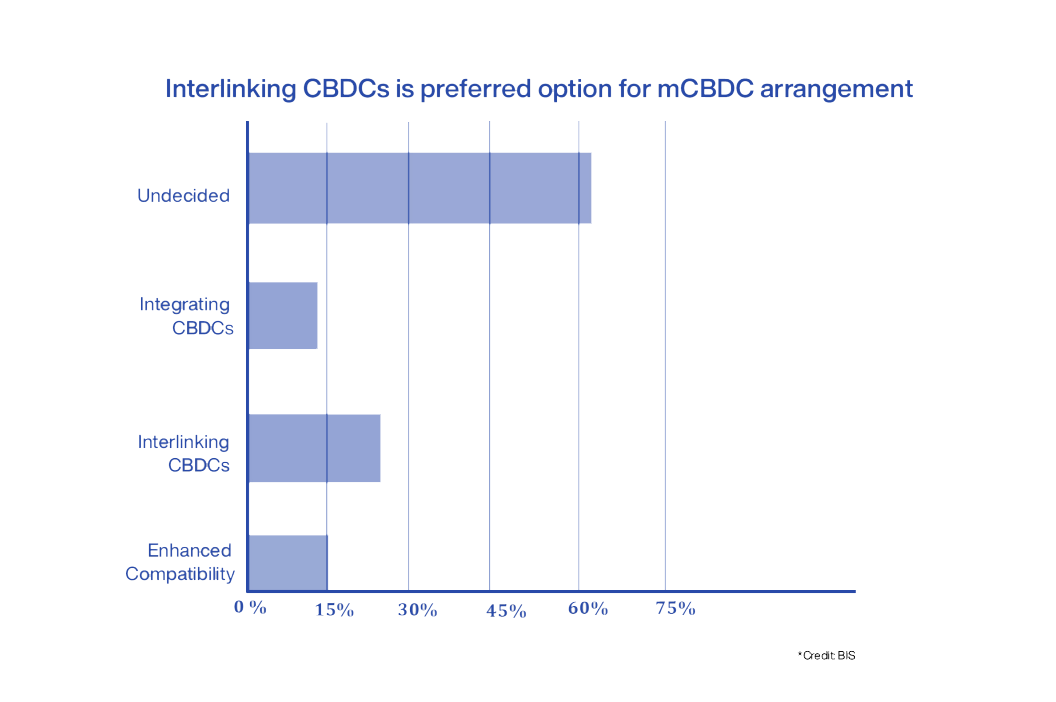

CBDC Arrangements: How Will it Work?

It has been observed that diversified choices and competitions have made cross-border payments quicker, cheaper, and more transparent. CBDCs are expected to offer more choices to consumers and an additional framework for financial institutions to fall back on and ensure seamless processes if one payment method system faces an outage. Moreover, to further understand how Cross Border Transactions will function in CBDC domains, it is vital to understand the functionality options in the Domestic Jurisdictions.

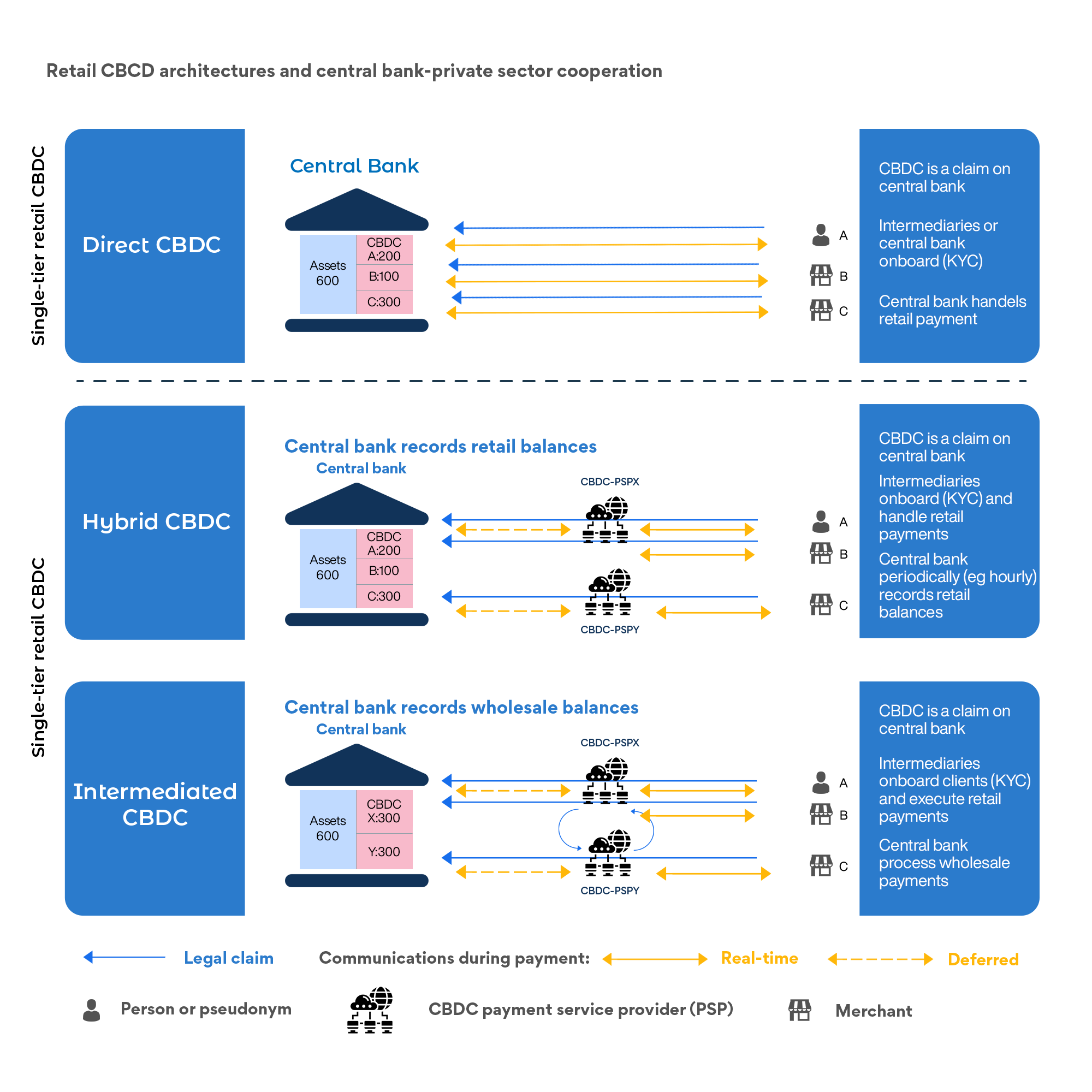

According to domain experts, central banks will have three framework options to introduce CBDCs; they are as follows:

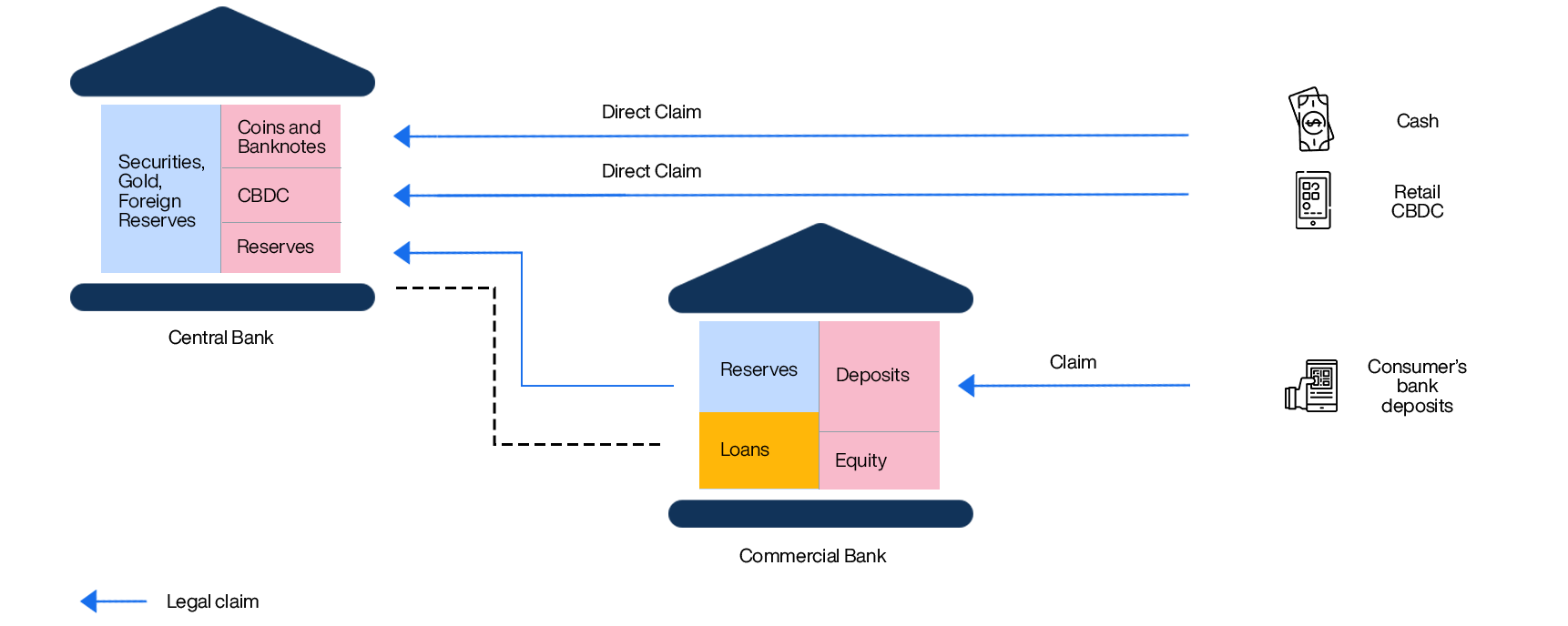

• Direct CBDC – A payment system operated by the Central Bank, which offers retail services. A CBDC is a direct claim on the Central Bank. The Central Bank maintains the ledger of all transactions and executes retail payments.

• Hybrid CBDC – An intermediate solution that runs on two engines. Intermediaries handle retail payments, but the CBDC is a direct claim on the Central Bank, which also keeps a central ledger of all transactions and operates a backup technical infrastructure allowing it to restart the payment system if intermediaries fail.

• Intermediated CBDC – An architecture similar to Hybrid CBDC, but in which the Central Bank maintains only a wholesale ledger rather than a central ledger of all retail transactions. Again, the CBDC is a claim on the Central Bank, and private intermediaries execute payments. For the purposes of this paper, this will be considered alongside the Hybrid model in our stocktake.

Source: BIS Working Papers No 880,

Even though many central banks are analyzing multiple technological alternatives concurrently, current proofs-of-concept favor distributed ledger technology (DLT) over established technical infrastructure.

Furthermore, Central Banks, especially the larger economies, are expected to take the hybrid route to introduce CBDCs in their jurisdictions. Hence it will be on the private sector to conduct all customer-facing transactions. Consequently, there will be similarities in domestic and cross-border CBDC frameworks. Furthermore, the pilot mCBDCs arrangement looks similar to traditional payment systems. As a result, adding mCBDC payment systems standards will reduce existing frictions and barriers that create hurdles in the smoother cross-border money transfer and cross-currency services.

Cross Border CBDC payment methods will work on common technical standards such as message formats, cryptographic techniques, data requirements, and user-friendly interfaces.

Added advantages will include aligned legal, regulatory, and supervisory standards. These attributes will result in simplified know-your-customer and transaction monitoring processes.

How are Payment Systems Managed Now?

Traditionally, managing Payment systems has been a complex task. The process of linking these systems is similar to connecting water pipes with different pressures or flow rates in a water distribution system.

In simple terms, joining together does not work; it is essential to install valves and controls. In the payment systems, Contractual and operational arrangements are equivalents to the valves and controls arrangements as mentioned in a water distributions system analogy. Therefore, this payment system agrees to take all the safeguard measures. A brief explanation for contractual and operational arrangements is presented herein for greater understanding :

• Contractual Relationship Arrangement– A contractual relationship is one in which one party, the agent, acts on behalf of another party, the principal. The agent may execute trades for the principal but is not responsible for the performance by the principal.

• Operational Accounts Arrangement – On the other hand, securities accounts are run by the Central Bank, in which credit institutions can place securities deemed suitable for the backing of central bank operations. The securities held on these accounts are finally deposited with the Central Securities Depository (CSD)* under the name of the National Central Bank (NCB), so that the transfer into a safe custody account results in a transfer between the bank's and the NCB's account with the CSD. The securities deposited with the NCB are generally pledged to the NCB as collateral for (interest-bearing) overnight and (interest-free) intraday Lombard loans. They can also be used for open market transactions (repos) based on a general authorization given to the NCB to acquire securities.

Multi-currency systems have used traditional money types to interlink. The domestic systems have a single independent rulebook, and the access criteria are somewhat different from interlinking, where participants directly connect to their home system.

Cross-border payments are transactions where the payee and the transaction recipient are based in separate countries. Thus they are more expensive and take longer to process than domestic payments due to the increased number of parties involved.

Integrating multiple CBDCs in a single mCBDC system

Multi-currency CBDC systems have significantly changed their designs from traditional payment systems to a modern one.

In this method, CBDCs could be issued onto a shared distributed ledger to attain economies of scale in development and maintenance. This design allows technical superiority over different interlinking systems. An example of this thought process is the Multi-CBDC Bridge project of the Bank of Thailand and Hong-Kong Monetary Authority. In this project, participants from two systems directly engage in a shared corridor network with a joint controlling operator, allowing participants to make cross-border payments through depository receipts* tied to CBDCs held in the domestic systems.

A depositary receipt is a negotiable certificate issued by a bank representing shares in a foreign company traded on a local stock exchange. Depositary receipt allows investors to hold shares in the equity of foreign countries and gives them an alternative to trading on an international market.

However, a single m-CBDC system raises a raft of policy issues for central banks. The broader implications of issuing a CBDC for monetary policy, financial stability, and payments policy will need to be worked through for each central bank. That will potentially require trade-offs in the final design, and this can be done only through a continuous linked settlement (CLS)*.

CLS continuous linked settlement is a cross-border payment system for settling foreign exchange trades that eliminates settlement risk through a payment versus payment mechanism. The CLS system is run by the CLS bank international, based in New York, holds the settlement members' accounts.

Source: BIS Working Papers No 880,

Aspects That Will Present a Challenge to mCBDC Policy Making

When considering a new system for settling foreign exchange transactions, central banks will face significant challenges. These concerns are natural as multiple jurisdictions will have policy issues, domestic compulsions, and an understanding of the subject.

However, to ensure that consumers can avail the benefits of an additional stable and cost-effective cross-border payments system, Central Banks and Policymakers will need to consider the following aspects for smoother incorporation:

1. Systemic risks,

2. Liquidity pressures,

3. Monetary policy,

4. International interdependencies,

5. Access for participants and currencies, and

6. Balancing the role of the private and public sector (CPSS.1996)*.

*CPSS (Committee on payment and settlement systems) consists of the central banks of G-10 countries. CPSS monitors developments in payments settlement and clearing systems to contribute to efficient payments and settlement systems.

M-CBDC bridge project

The multiple CBDC or m-CBDC Bridge is a wholesale central bank digital currency Co-creation project involving the BIS innovation hub, the Hong Kong monetary fund authority and Bank of Thailand, the digital currency people's Bank of China, the UAE. In February 2021, it proposed solutions and concepts to alleviate the current pain points in cross-border fund transfers. There are the following points to existing pain points.

● Inefficiencies

● High costs

● Complex requirements for regulatory compliance

The m-CBDC bridge project was envisaged to deliver faster and transparent cross-border funds and payments. The project has since been renamed the Inthanon-Lion Rock project. It collaborates with the Bank of Thailand and Hong-Kong monetary authority (2020), the Digital currency institute, the People's Bank of China, and the Central Bank of UAE.

BIS or bank of innovation hub intends to contribute to this area through applied technology research, proof of concept, and prototypes with central banks worldwide.

The m-CBDC bridge project fosters a conducive environment for more central banks in Asia and other regions to jointly study the potential for DLT. They are also eager to enhance the financial infrastructure for cross-border payments. Multi-CBDC Bridge project focuses on the multi-currency system, which was used recently by the central and commercial banks to streamline key financial-economic and regulatory activities.

Central and commercial banks have triggered liquidity saving mechanisms to relieve gridlock between networks & stakeholders within a single local jurisdiction. Multi-CBDC Bridge and central banks automate critical regulatory operations such as monitoring bank wallets and transactions in real-time and setting threshold limits for their currency. These actions help reduce the balance of commercial banks withholding the limits.

Here is how it can be done:

Commercial banks from different countries set up inter-bank current accounts with each other. However, with more and more commercial banks on-boarded, the implementation cost will increase significantly.

* Distributed ledger technology (DLT) is a digital system for recording the transaction of assets in which the transactions and their details are recorded in multiple places simultaneously.

It refers to the technological infrastructure and protocols that allow simultaneous access, validation, and record updating in an immutable manner across a network spread across multiple entities or locations.

By implementing an m-CBDC Bridge, two commercial banks from different countries can perform real-time peer-to-peer trading. This capability enhancement fundamental goal of deploying digital currency in cross-border payments. Achievement of this goal will allow the optimisation of the existing corresponding banking model.

The Ethereum blockchain technology and M-CBDC Bridge explored the future capabilities with the help of Distributed ledger technology. It allowed the development of a POC (proof of concept) prototype to support real-time, cross-border, foreign exchange payment and transactions with the help of multiple jurisdictions. Furthermore, it helped in analysing business use cases and cross-border contexts with domestic and foreign currencies.

Representative proposed solutions include:

● Commercial banks from different countries adopt the same super-sovereign digital currency for cross-border payments, such as the multi-currency stable coin Libra/Diem. However, this depends on the market acceptance of the super-sovereign digital currency and its ability to perform the essential functions of currency. Although, this procedure may create monetary sovereignty issues between countries.

● Commercial banks from different countries adopt some major CBDC or stable coin for cross-border payments such as digital USD or USD stable coin. However, this will result in stronger currencies substituting weaker ones.

● Different countries issue CBDC on their own DLT and achieve cross-chain interoperability via smart contracts to achieve PvP. However, the low maturity level of existing cross-chain technologies limits the application of this model.

In more straightforward terms, a central bank digital currency or CBDC must be used by individuals to pay businesses, shops, or each other with a retail CBDC or used between financial institutions to settle trades. This attribute is one of the fundamental features of money, wherein it is accepted as a means of value and exchange.

In financial markets where we expect to witness wholesale CBDC use cases, the Central banks need to explore whether it will help them achieve their good public objectives, such as

1. Safeguarding public interest money

2. Maintaining financial stability and

3. Ensuring safe and resilient payment systems and infrastructure.

However, if these safeguards are measured digitally, the general public will retain access to the safest form of money or a claim on a central bank. In addition, the digitisation process could promote diversity in payment options to make cross-border payments faster and cheaper, increasing financial inclusion and possibly facilitating fiscal transfers in times of economic crisis.

Central and commercial banks have triggered liquidity saving mechanisms to relieve gridlock between networks & stakeholders within a single local jurisdiction. Multi-CBDC Bridge and central banks automate critical regulatory operations such as monitoring bank wallets and transactions in real-time and setting threshold limits for their currency. These actions help reduce the balance of commercial banks withholding the limits.

Coordination needs m-CBDC arrangements.

The BIS is supporting experimentation on m-CBDC arrangements through its innovation Hub. Furthermore, by 2022, it aims to explore PoC(proof of concept) towards linking m-CBDC with different currencies to allow for PvP settlement.

The Challenges it might Face

Exchange Rate Conversion has the potential of creating conflict for any m-CBDC arrangement. In the current scenario, FX wholesale markets are vast and complex, and they are fragmented and concentrated among very few large dealers. This situation creates the need for improvements in the existing arrangement that the interlinking of systems can achieve. For example, all FX settlements must be PvP by default, rather than requiring routing or specific settlement instructions through an interface.

Trading venues will be required to be integrated with the m-CBDC systems. This action will further help to reduce the complexity, fragmentation, and concentration of currency markets (Bank of Thailand and Hong Kong Monetary Authority).

This model is also adopted in Project Aber SAMA and CBUAE (Central Bank of the United Arab Emirates)*, which takes a step further via joint issuance of a CBDC used in the single mCBDC arrangement. Since the Saudi Riyal and the UAE Dirham are pegged to the US dollar, the newly issued CBDC has effectively guaranteed a fixed exchange rate to both of the local currencies.

*Excerpts from the report on Project Aber: Joint Digital Currency and Distributed Ledger proof of concept in the year 2020 The Saudi Central Bank (SAMA) and Central Bank of United Arab Emirates (CBUAE)

The Technology

On the other hand, different countries are developing their forms of digital currency; Some are using existing blockchain technology, and In contrast, others are designing or working on their own. However, a large number of Central Banks are working on related projects, and some are in the advanced planning stages of launching their digital currency.

Although multiple Central Banks believe that the Blockchain network is not the only technology for introducing Digital Currencies; However, various proof of concepts point to the fact that it is the most suitable of all the options available for developing the CBDC technology framework.

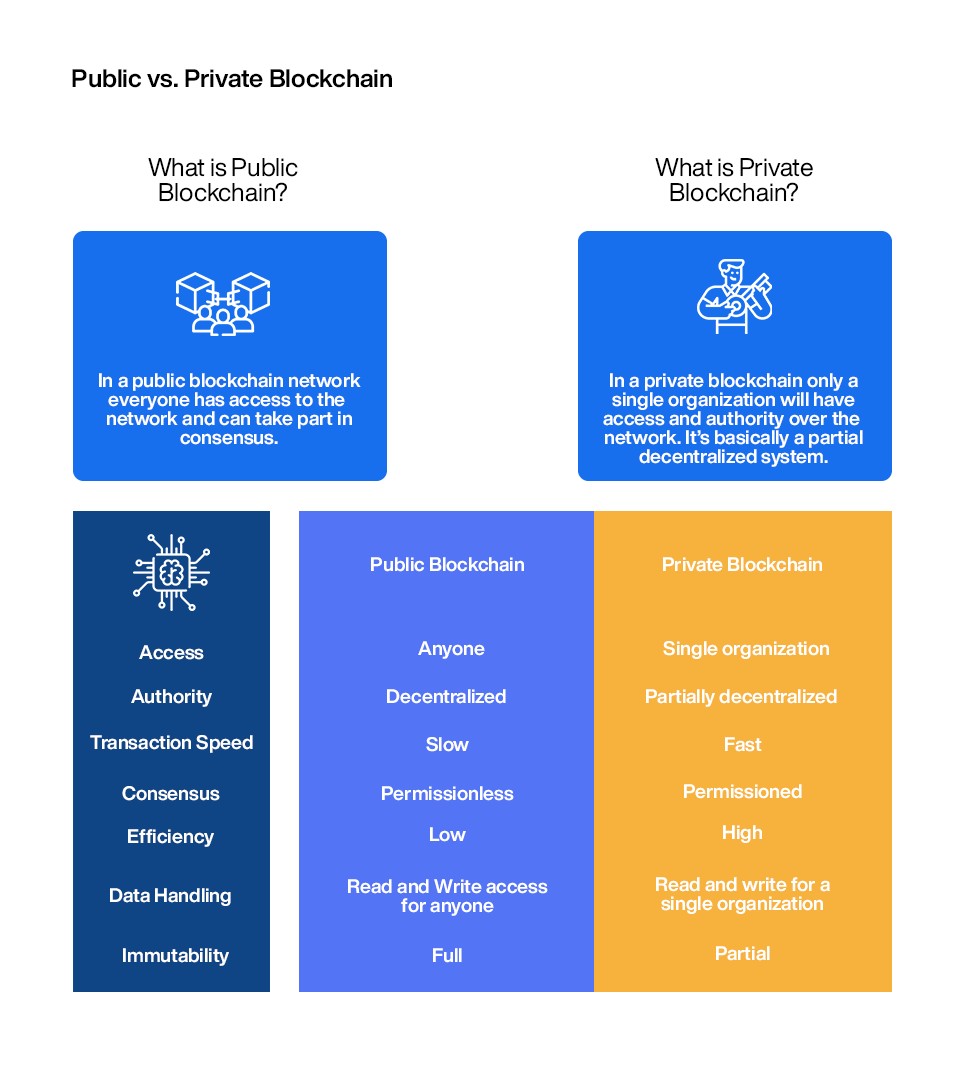

Furthermore, Blockchain Networks that various stakeholders are contemplating can be broadly be classified into two parts, that are:

1. Public Blockchains

2. Private Blockchains

A public blockchain is permitted to all, and any entity can join the arrangement. Each member on the chain can access, read and write actions. Since it is decentralised and wholly distributed, every node confirms to approve any action. Data cannot be modified or manipulated once it is placed on the block.

Wherein a private blockchain puts limitations on who is joining the network. A user is allowed access only by the network initiator or by a predefined set of rules. Once the user is granted consent, it can perform the same duties as that of other users.

According to Dr. Nir Kshetri, a professor at the University of North Carolina-GreensboroPrivate blockchains are more efficient. As a result, they may perform better than public blockchains in terms of privacy protection

Use Cases

In the Middle East, the central banks of Saudi Arabia and the United Arab Emirates announced the results of their proof of concept to test the viability of a shared digital currency between the two countries. In the light of the new experiments and researches, both central banks led this project as an innovative, driven initiative. The initiative sought to explore whether distributed ledger technology could enable cross-border payments between the two countries to be re-imagined: using a new, dual-issued digital currency as a unit of settlement between commercial banks in the two countries and domestically. The name Aber was selected because, as the Arabic word, for 'crossing boundaries,' it captures the cross-border nature of the project and our hope that it would also cross boundaries in terms of the use of the technology.

Dr. Nir KshetriBridge technologies are likely to dramatically impact currencies and markets by helping produce trust in parties involved in a transaction.

Although using a blockchain-based settlement interface, the assets on the distributed ledger relate to the payments, thereby reducing risk. China's DCEP's (Digital Currency Electronic payment) interoperability with other tokens and blockchains can allow Chinese companies and their foreign trading partners to move money across borders without depending on US dollars as an intermediary. The bridge technology - mCBDC Bridge can increase China's international trade efficiency and made its supply chains highly efficient.

Deepika Bawa

deepika@agpaytech.co.uk

Senior Research associate

Srijita Mukherjee

srijita@agpaytech.co.uk

Research associate